LONG-TERM REPRICING POTENTIAL

The CCR comprises Prime Districts 9, 10, 11, the Downtown Core and Sentosa, and is viewed as a proxy for high-end and luxury homes. The RCR consists of areas within the Central Region, excluding the CCR and includes areas such as Queenstown, Toa Payoh and Bishan, which are city-fringe areas. The OCR consists of the rest of the island and reflects suburban housing areas.

Singapore condo market (including both condominiums and apartments) capped off a robust 2022 with overall prices up by 8.1 per cent year on year, notwithstanding two rounds of cooling measures over the last two years. However, price growth differed across market segments, with condo prices in the Rest of Central Region (RCR) and Outside Central Region (OCR) locking in growth of 9.7 per cent and 9.3 per cent year on year respectively in 2022, while Core Central Region (CCR) prices grew only 4.8 per cent year on year.

PRICE GAP NARROWING

The CCR underperformance has led to a narrowing price gap between CCR condos vis-a-vis the RCR and OCR counterparts, based on analysis of caveat data (data comprises non-landed transactions, 99-year leasehold) for new launches from 2008 till 2023.

As shown in the chart below, avg. RCR prices are now inching close to CCR prices which make projects in CCR that are offering discounts very favourable and good value.

RENTAL YIELDS HAVE GONE UP

While CCR condo price growth has strongly lagged, CCR rental growth has been more promising. CCR condo rents grew by 28.2 per cent in 2022, comparable to RCR and OCR year-on-year rental growth of 30.3 per cent and 31.8 per cent respectively.

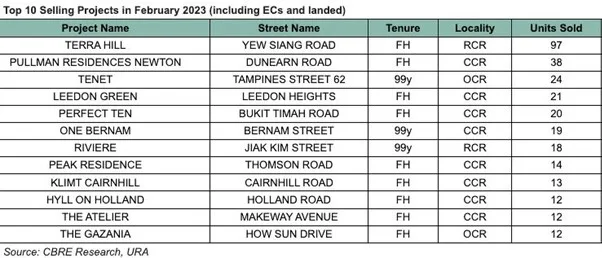

TRENDING NOW ARE CCR PROJECTS

With no new launches, out of the 12 top selling projects in Singapore for Feb, 8 are from CCR mainly due to the discounts that are being offered. Together with the reasons highlighted above, buyers are finding more value in purchasing CCR project now.

CONCLUSION

Given the narrowing price gap, higher rental yields, relatively limited supply and expected increase in demand, CCR prices could surprise on the upside over the next five years. With private residential prices at historical peaks and still expected to trend higher in 2023, the value proposition of CCR properties looks increasingly attractive.